Connect with Us! Use Our Futures Trading Levels and Economic Reports RSS Feed.

![]()

![]()

![]()

![]()

![]()

![]()

1. Market Commentary

2. Futures Support and Resistance Levels – S&P, Nasdaq, Dow Jones, Russell 2000, Dollar Index

3. Commodities Support and Resistance Levels – Gold, Euro, Crude Oil, T-Bonds

4. Commodities Support and Resistance Levels – Corn, Wheat, Beans, Silver

5. Futures Economic Reports for Friday May 30, 2014

Hello Traders,

For 2014 I would like to wish all of you discipline and patience in your trading!

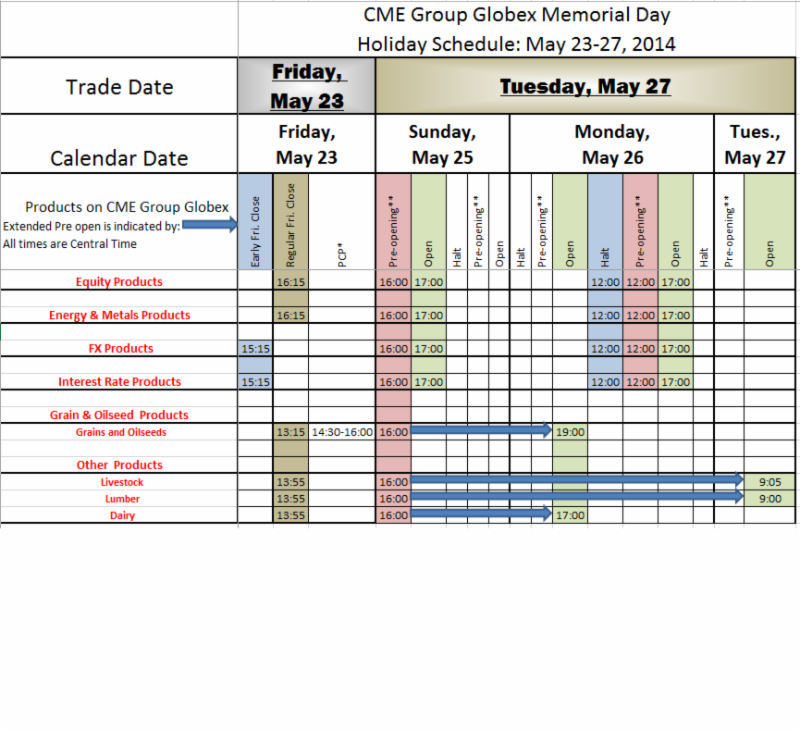

US Bonds front month as of tomorrow is SEPTEMBER~ ZB U4.

FRONT month for gold is AUGUST GC Q4 or GGC Q4.

Indices and Currencies are still trading the June contract.

Excellent and interesting resource for those of you who step out of the day-trading world, courtesy of www.MRCI.com :

http://www.mrci.com/special/correl.htm

Of course, one would expect gold and silver futures to move in tandem, to correlate closely, with each other. They’re both precious metals, aren’t they? But silver is also a by product of copper mining. Would they tend to trade together-or contrarily?

Similarly, one might expect price activity in Euros and T-bonds to be similar. Conversely, the Swiss Franc and the Dollar Index should have opposite reactions to the same market input.

A primary rationale behind the continuing bull market in stocks has been declining interest rates. How closely, in fact, have T-bond and SP500 futures tracked each other on a daily basis?

For years traders have made a very non-fundamental connection between the silver and soybean markets. How closely have they traded?

Heating oil and crude oil-yes. But live cattle and the J-Yen???

Some brief explanation is required. The singular relationship under consideration is the frequency of duplicated up/down daily closings. E.g., if Market A closed higher on Day 1, did also Market B? (In that respect, the study is qualitative, not quantitative, i.e., the amount is irrelevant.)

Without going into further details of least-squares and scatterplots, the precise statistical terminology that describes each relationship is a sample coefficient of correlation, a number greater than -1 and less than +1. Thus, if, every day over the sample period, each of two markets duplicated the other’s higher or lower closing, they would have a coefficient of correlation equal to 1/1, or +1. Conversely, two markets that always closed contrarily to each other would have a coefficient equal to -1. A 0 value indicates no correlation whatsoever. For convenience, however, all values in the spread sheet have been stated in terms of percentages of +1 or -1.

Remember, the amount of change is irrelevant, which can account for differences in trend.